Global RF Circulator Market Outlook 2026: Growth, Challenges, and Key Players

Updated on:

Keywords: RF circulator, isolator, RF circulator market 2025, isolator market outlook

Introduction and Scope

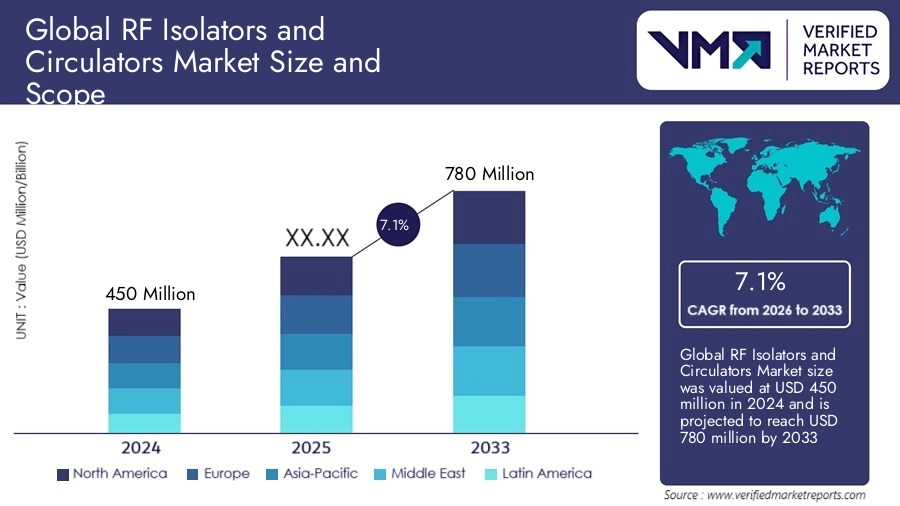

The RF circulator and isolator market enters 2025 at an inflection point. Defense radar recapitalization, expanding LEO/MEO satellite constellations, and densifying 5G/early‑6G infrastructure continue to pull demand across microstrip, coaxial, and waveguide formats. At the same time, cost pressure, rare‑earth ferrite volatility, and qualification bottlenecks create friction for both Tier‑1 integrators and emerging vendors. This outlook distills growth vectors, headwinds, technology trajectories, and the key players shaping competitive dynamics in 2025.

We keep the analysis vendor‑neutral and engineering‑grounded. Instead of single‑number forecasts, we present scenario bands and qualitative indicators that help program managers, sourcing teams, and design engineers triangulate volumes, prices, and lead‑time risk for RF circulators and isolators across L/S/C/X/Ku/Ka bands.

TDK: Title/Description/Keywords are embedded in <head>; canonical is set.

1) Executive summary: where growth meets constraint

- Demand: Radar recapitalization and SATCOM payloads support steady growth; private 5G and FR1 macro densification continue, with exploratory FR2 nodes for fixed wireless and campus networks.

- Technology: Continued push for low insertion loss, higher isolation, and miniaturization in drop‑in/microstrip; waveguide remains essential for high‑power/space payloads.

- Constraints: Ferrite supply and magnet grade swings, precision machining capacity, and environmental test backlogs keep lead times sensitive.

- Pricing/ASP: Stable to slightly up in defense/space; mixed in commercial telecom depending on lot sizes and localization of supply.

Tips:

Budget with scenario bands instead of single‑point estimates; validate with rolling vendor RFQs.

2) Demand drivers by vertical

- Defense radar & EW: Multi‑band AESA upgrades and lifecycle resets drive volumes in drop‑in and waveguide circulators. Emphasis on high power, temperature stability, and qualification data packs.

- Satellite communications: LEO/MEO constellations add steady demand in X/Ku/Ka for payload and ground terminals. Reliability and radiation tolerance push suppliers toward conservative IL and margin policies.

- 5G/early‑6G: Macro and small‑cell deployments sustain microstrip/coaxial components. Private networks require ruggedized designs with constrained IL to protect PA efficiency.

- Test & measurement: Vector network analyzers, signal chains in PA benches, and production handlers use internal isolators to stabilize measurements.

3) Technology and packaging trends

- Drop‑in/microstrip: Packaging improvements (low‑roughness copper, high‑Q plating, adhesive control) cut insertion loss while improving yield. Thermal vias and metal backs enhance power dissipation.

- Coaxial: Remains favored where connectorized convenience and quick swapping trump footprint. Precision alignment and ferrite geometry minimize mode conversion.

- Waveguide: Retains leadership in high‑power radar and satellite payloads; choke grooves and surface finish reduce wall loss, enabling low IL at kW levels.

- Materials: Narrow‑linewidth ferrites and stable magnet grades curb magnetic loss and drift; interest in process‑controlled YIG‑family ferrites for upper‑band performance.

4) Regional landscape: Americas, EMEA, and APAC

Americas emphasize radar modernization and commercial SATCOM ground terminals. EMEA shows healthy defense electronics investment and selective telecom rollouts. APAC leads in telecom volume and increasingly in space programs, with competitive local supply chains for microstrip and drop‑in formats. Export regimes and compliance frameworks influence cross‑border sourcing and dual‑use shipments.

5) Competitive map and key players (indicative)

The vendor landscape spans global incumbents, regional specialists, and custom R&D houses. Incumbents dominate waveguide and space‑qualified parts; agile firms compete aggressively in microstrip and drop‑in with fast customization. Buyers should evaluate: depth of materials control (ferrite, magnet), in‑house machining/plating, environmental test capacity, and statistical process control (Cp/Cpk) for IL and isolation.

- Global incumbents: Strong heritage in waveguide/coaxial, space and defense programs, broad qualification libraries.

- Regional specialists: Fast‑turn engineering for custom bands, competitive in drop‑in and microstrip, often flexible MOQs.

- Custom/OEM partners: Joint development for unique apertures and thermal constraints, with lifecycle support and obsolescence planning.

Note: We keep names generic to remain neutral; procurement teams should triangulate vendor fit via pilot lots, design of experiments, and test‑to‑fail data.

6) Supply‑chain realities: ferrites, magnets, machining

Ferrite powder chemistry, sintering lines, and magnet grades (including high‑temperature variants) remain the heartbeat of capacity. Precision machining for junctions and housings, plus high‑Q plating queues, create bottlenecks in peak cycles. Adhesive selection and bond‑line control are frequently overlooked levers that affect both insertion loss variability and thermal survivability.

7) Pricing and ASP trends

Defense and space programs maintain premium ASPs tied to documentation, qualification, and lot‑level testing. Telecom sees a mix: volume microstrip parts face cost pressure, while specialty bands and tighter IL specs command a premium. Localized production and alternative material sourcing stabilize some price swings, but complex bills of materials (multiple ferrite tiles, magnet stacks, precision fasteners) limit dramatic declines.

8) Risks and challenges in 2025

- Lead‑time volatility: Environmental test backlogs and magnet grade availability can shift delivery windows by weeks.

- Qualification burden: MIL/space‑level evidence packages and re‑qualification for minor design changes tax engineering bandwidth.

- Miniaturization penalty: Pushing size down often nudges IL up; bandwidth targets exacerbate the trade‑off.

- Talent and fixture limits: Senior RF/magnetics engineers and high‑frequency fixturing for TRL/SOLT de‑embedding remain scarce in some regions.

9) Scenarios for 2025: base, upside, and downside

- Base case: Mid‑single‑digit growth as radar and SATCOM offset uneven telecom CAPEX; ASPs broadly stable.

- Upside: Accelerated LEO ground terminal deployment and defense appropriations lift orders, with modest ASP expansion for low‑IL/high‑power SKUs.

- Downside: Procurement pauses or supply disruptions elongate lead times and compress margins; non‑critical telecom volumes soften.

10) What buyers should do now: a procurement checklist

Data & Performance

- Swept IL/Isolation/VSWR curves across guaranteed bandwidth

- Phase linearity / group delay ripple targets

- Average & peak power ratings with waveform assumptions

Build & Materials

- Ferrite linewidth (ΔH), magnet grade, bias uniformity

- Plating stack, surface roughness on current paths

- Bond‑line thickness control, CTE alignment

Reliability & Supply

- MIL/space qualification data; burn‑in and reverse‑power soak

- Cp/Cpk for IL and isolation; change‑control process

- Second‑source plan for ferrites and magnets

Conclusion

The 2025 RF circulator and isolator market blends durable defense/space demand with disciplined telecom investment. Technology progress is steady, not explosive: lower insertion loss, tighter isolation, and smarter thermal paths. Supply‑chain limits and qualification rigor remain the gating factors. Teams that standardize packages, lock materials early, and instrument vendors with data‑rich trials will manage price, lead time, and performance risk more effectively than peers.

FAQ

Will FR2/6G dramatically expand circulator volumes in 2025?

Not dramatically in 2025. Growth is steady; major inflections are more likely beyond 2026 as use‑cases and infrastructure mature.

Which packages will grow fastest?

Microstrip/drop‑in in telecom and tactical systems by unit volume; waveguide in high‑power radar and satellite payloads by value.

Can a circulator be replaced by solid‑state non‑reciprocal alternatives?

Research is active, but ferrite‑based devices continue to lead for high power, bandwidth, and ruggedness in 2025 deployments.

How do I compare vendor quotes accurately?

Normalize IL/Isolation to the same bandwidth and temperature, align peak power assumptions (pulse width/duty), and review process controls and test evidence.

What is a realistic IL target for telecom microstrip?

Roughly 0.3–0.6 dB typical across band, depending on bandwidth and board stack‑up; premium designs can do better with cost/size trade‑offs.

Relateds

About the Author

HzBeat Editorial Content Team

Jason is a seasoned RF Engineer with over [8] years of experience, specializing in the design and development of RF front-end modules, antenna systems, and high-frequency circuits. He is proficient in the entire product lifecycle, from concept definition and simulation optimization to prototype testing and mass production.