Procurement Wars: 5G Operators Compete for Limited RF Isolator Suppliers

Updated on:

Keywords: RF Isolator Suppliers, Procurement of RF Isolators, RF Isolators For 5g Operators

Introduction

As 5G rollouts enter densification and mid‑band expansion, rf isolator supply has become a bottleneck. These rf components protect high‑power PAs and sensitive LNAs from reverse energy in massive‑MIMO radios and small‑cell nodes. With limited qualified suppliers, operators increasingly face procurement battles for long‑lead inventory, qualification slots, and engineering support.

This report synthesizes public, citable sources (3GPP/GSMA, IEEE, Allied/Technavio, ECSS/NASA/NRL) and adds system‑level context for telecom buyers.

5G cell tower (2024). Source: Wikimedia Commons/Marcin Floryan (CC BY-SA 4.0). File page linked via Special:FilePath.

Market Landscape & Capacity Constraints

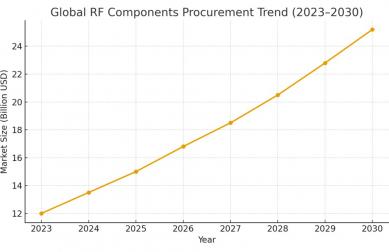

Analysts project steady growth in the isolator segment through 2030, driven by 5G/6G infrastructure and defense/satcom spill‑overs. Industry reports indicate that market value for rf isolator categories (coaxial, microstrip/SMT, waveguide) is set to expand at mid‑single‑digit CAGRs, with mid‑band (n77/n78) deployments consuming large volumes of SMT isolators while mmWave backhaul and satcom gateways drive high‑power waveguide needs. Note: precise values vary by report and year; see Allied Market Research and Technavio for the latest figures.

Vodafone 5G site in Germany (2019). Source: Wikimedia Commons (CC BY-SA 4.0). File page linked via Special:FilePath.

Why Supply Is Tight: Technical & Industrial Causes

- Ferrite material & magnet stacks — High‑quality garnet ferrites and stable magnets require controlled sourcing and machining tolerances; yields and cycle times limit ramp speed.

- Qualification & reliability testing — Operators require proven isolation, insertion loss, and VSWR across temperature/humidity; for aerospace backhaul, ECSS‑aligned evidence (multipaction/EMC) further extends lead times.

- Form‑factor mix — SMT/LTCC parts scale in high volume but need tight line control; waveguide and drop‑in variants remain labor‑intensive.

- Competing verticals — Defense radar and satcom payloads compete for the same experienced suppliers, pulling capacity during program peaks.

Supply chain flow. Source: Wikimedia Commons (CC BY-SA 3.0). Useful to visualize upstream supplier bottlenecks.

How 5G Operators Compete: Procurement Strategies

- Qualification pipelines — Run parallel supplier qualifications (A/B sourcing) to secure second sources. Require S‑parameters over temperature, derating curves, and FAIs for target SKUs.

- Vendor‑managed inventory — Negotiate buffer stock at rf components distributors; align replenishment with radio rollout waves.

- Design‑to‑order — For high‑power or unusual duplexing needs, co‑design with vendors (mechanical envelope, flange/interface, thermal path) to reduce rework risk.

- Calendar discipline — Lock forecasts early; chase long‑lead ferrite and magnets first, then housing/machining and screening slots.

- Total cost & risk — Consider lifetime OPEX: higher isolation and lower loss reduce PA stress and energy costs over the network life.

5G mobile cell truck setup (U.S. Air Force photo, public domain). Source: Wikimedia Commons.

Supplier Landscape & Hzbeat Links

The supplier landscape remains concentrated among experienced ferrite and LTCC houses. Buyers typically split needs by form factor and power class:

- SMT/LTCC isolators for n77/n78 radios and small cells — focus on low loss and repeatability.

- Waveguide & drop‑in isolators for high‑power backhaul, gateways, or radar spill‑overs — prioritize isolation margin and thermal performance.

For detailed specifications and custom requests, see Hzbeat products and contact pages:

- Hzbeat Coaxial Isolator — catalog options for base‑station and lab builds.

- Hzbeat Waveguide Isolator — high‑power flange families up to mmWave.

- Contact Hzbeat — for design‑to‑order, qualification support, and forecast planning.

Outlook: 2025–2028

- Mid‑band densification sustains SMT/LTCC volumes; operators increasingly seek predictable loss/isolation vs. temperature data.

- Backhaul & NTN keep waveguide demand resilient; aerospace screening knowledge diffuses into telecom acceptance criteria.

- Energy efficiency pressures favor low‑loss parts to curb PA overdrive and lower site OPEX.

- Second‑source normalization — dual‑qualified parts become standard to minimize outage risk.

FAQ

Q1: What makes an isolator “5G‑ready”?

A: Stable isolation and low insertion loss across the operating band and temperature; proven reliability data; SMT coplanarity/flatness for array assembly.

Q2: How long are current lead times?

A: Highly variable; ferrite/waveguide SKUs often carry longer machining and screening cycles than SMT/LTCC. Engage suppliers early with forecasts.

Q3: Can a waveguide part replace SMT?

A: No. Match the form factor to power class and integration constraints; waveguide suits high‑power backhaul/gateways, SMT/LTCC suits radio arrays.

References

- 3GPP & GSMA publications on 5G deployment and mid‑band spectrum usage.

- Allied Market Research — RF isolator/5G infrastructure market outlook (latest editions).

- Technavio — RF components and isolators, vendor analysis (latest editions).

- IEEE Transactions on Microwave Theory and Techniques — non‑reciprocal devices and isolator design papers.

- ECSS‑E‑20‑01A Rev.1 — Multipaction design and test (space programs).

- ECSS‑E‑ST‑20‑07C Rev.2 — Electromagnetic compatibility (space programs).

- NASA NTRS & U.S. NRL — historical/technical studies on waveguide non‑reciprocal devices.

Relateds

About the Author

HzBeat Editorial Content Team

Marketing Director, Chengdu Hertz Electronic Technology Co., Ltd. (Hzbeat)

Keith has over 18 years in the RF components industry, focusing on the intersection of technology, healthcare applications, and global market trends.